The one small-cap tech stock I recommended to readers more than any other over 2016 and 2017 was aerial-mapping business Nearmap Ltd (ASX: NEA).

Fortunately it turned out to be the best performing stock over 2018 from the S&P/ASX 300 Index, with other top performers including Bravura Solutions Ltd (ASX: BVS) and Jumbo Interactive Ltd (ASX: JIN).

So let's consider where Nearmap might head in 2019.

In fairness neither Nearmap's income statement or cash flow statement for FY 2018 impress, with an operating cash loss of $2.7 million on revenue of $64.2 million.

While total cash outflows hit $10.6 million for the year largely on the back of $9.5 million in investing costs related to development ($5.7 million) and property and equipment investment ($4.1 million).

The income statement printed a full year accounting loss of $11 million on $54 million of trailing revenue.

However, in the share market it's the future that counts and Nearmap's software-as-a-service (SaaS) business model and strong growth suggest it's close to delivering growing profits for investors, while operating in a large addressable market.

As at September 30 2019 it had more than $70 million in annualised contracted value (ACV), with the lifetime value (LTV) (average revenue per user (ARPU) multiplied by number of subscribers and adjusted for gross margin & churn) of the portfolio at $715 million.

In other words Nearmap has $715 million of future revenue "locked in" assuming churn (the number of customers that leave every year as a percentage of the total) and gross profit margin stays the same.

In FY 2018 12-month churn stood at a modestly high 7.5% and gross margin (GM) 81% in calculating the $715 million LTV figure.

Notably, Nearmap's GM at its maturer Australian business sits at 94% and group GM should improve thanks to its SaaS business model, while the churn of 7.5% also leaves room for improvement.

So we know that if the business continues to grow subscriptions, ARPU and gross margin at healthy rates while managing costs then it should grow profits at strong compound rates over say 3 to 6 years.

And at the end of the day, share prices always follow profits higher or lower in time.

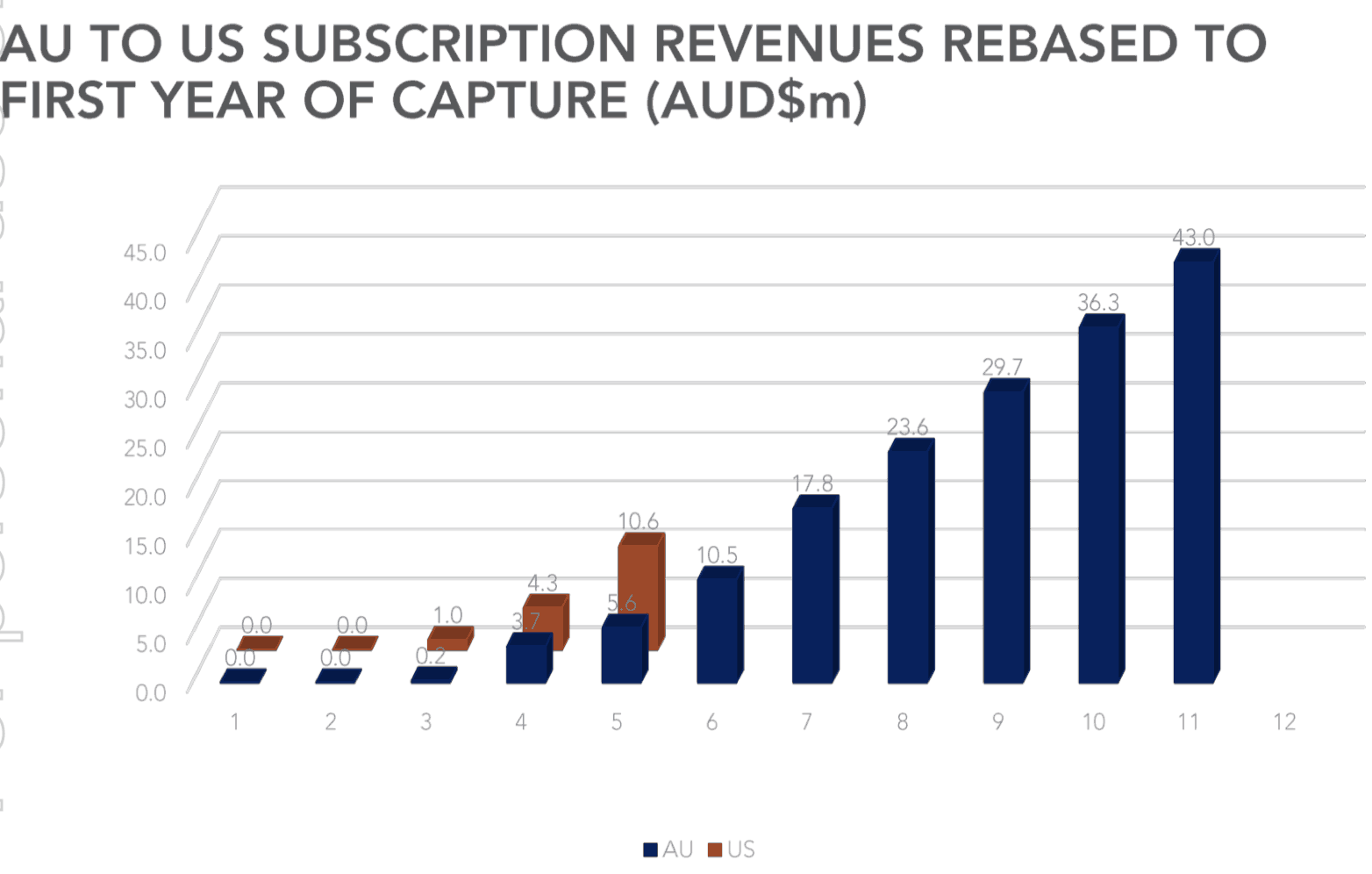

Much of the expectation for Nearmap's success is pinned on its potential in the U.S. market and below is a chart that shows its progress growing revenue in the U.S. compared to Australia, since it launched in the U.S. a few years ago.

Source: Nearmap investor presentation November 15, 2018.

As you can see if Nearmap keeps growing strongly in the U.S. the future looks good and progress under its U.S. head Patrick Quigley and group CEO Rob Newman has been strong over the past 12 months.

Valuation

Nearmap has 442.4 million shares on issue and a market value of $699 million based on today's share price of $1.58.

That's around 10x current ACV with Nearmap expecting to breakeven in 2019.

It trades on more like 8x enterprise value (EV) to ACV after we adjust for an estimated $87 million in net cash on hand and no debt following a $70 million capital raising last September.

In valuing SaaS businesses there are dozens of inputs to consider including profitability, competitive position, growth rates, churn, etc, (a whole new article), but Nearmap looks reasonable value to me versus some of its SaaS peers.

On a $699 million market cap it also has room to grow (versus a SaaS business already worth $2 billion for example) if it executes on its growth plans in Australia, the U.S. and now Canada.

However, it remains a high-risk bet, as it's vulnerable to competition from powerful tech companies like Google, while its failure to post a profit also means it's probably not your mum and dad's idea of a good investment.

There's also the specific risk that the U.S. business turns into a money pit for multiple reasons in which case the share price would fall fast.

Still, I expect Nearmap shares could soar again in 2019 if it executes and then, inter alia, comes on the radar of more institutional investors.